Partial Portfolio Update: Three Catalysts, Two Interviews and an Exit

$AIRDF $CISO $CHHYF $LEEEF $GOAT $MDNAF $AMFN

Lots’s of emails coming from me this week, apologies in advance there is a lot happening.

Partial Portfolio Update: Two Interviews, Three Catalysts, and an Exit

Two CEO conversations posted this week, an annual print I think matters more than the stock reflects, a Q1 cannabis earnings call landing tomorrow, an ASCO presentation at the end of May, and a swing trade I’ve closed out completely, for now. Here’s where my head is on each.

Rocket Doctor AI (CSE: AIDR | OTC: AIRDF) — The Gap Between Built and Booked

The company posted $1.74M in annual revenue, with Q4 coming in at $697,340… over 30% quarter-over-quarter growth, marking the third consecutive sequential growth quarter. Gross margin held at 84% in Q4. The Canadian operation has now powered more than 750,000 patient visits to date.

Here’s the piece I keep coming back to: U.S. operations represented less than 3% of 2025 revenue. And yet, through Q4 2025 and Q1 2026, Rocket Doctor finalized in-network agreements covering over 21 million lives across California, New York, and Maryland, spanning commercial, Medicare Advantage, Medicaid, and Veterans populations. The U.S. payer infrastructure is in place. The revenue from those covered lives is, by and large, not yet reflected in the 2025 numbers.

This is a digital health platform and marketplace, and the gap between what’s already built and what’s already booked is the structural setup the company is now executing into.

Expect a full article on Rocket Doctor in the next couple days.

CISO Global (NASDAQ: CISO) — The Hard One

I posted my conversation with CISO CEO Dave Jemmett this week. If you own this stock, please watch the full interview. I’m not going to summarize the whole thing here, but I do want to flag a few things upfront.

I covered CISO from around fifty cents up to its peak of about $1.70. We’re now sitting around thirty cents. A lot of long-term holders are still in it, and a lot of them have asked me what I think.

The honest answer is in the video. I show my work, Dave answers the questions I had, and you get to decide what fits your situation. What I’ll say here is what’s changed since November and what hasn’t:

What’s changed. The April no-action letter to the SEC is filed, that’s the reason for the five-month communication blackout, which Dave addresses directly. The B. Riley facility has had no additional draws. New sales leadership is in place specifically to fix the channel program, and per Dave, two new clients have signed (one of which most listeners would recognize, but the company can’t name without permission).

What hasn’t. The stock is under a dollar against a NASDAQ listing requirement. Dave was unequivocal in the interview that there will not be a reverse split, which answers a question a lot of you have asked me directly. Insider buying hasn’t happened, and Dave’s reason (he’s already personally funded most of the company through uplist, and has been deferring bonuses for years) is the kind of thing I want shareholders to hear in his own words rather than secondhand from me.

I’m still long. I am not adding here, I am not selling here. Different investors have different risk tolerances, and underwater holders should not make decisions based on what someone else is doing with their position. This is the kind of stock where “your money, your call, your responsibility” actually means something.

The full conversation is below. I’d particularly point you to the section on the no-action letter and the securities lending framework, that’s substantive and most retail holders haven’t engaged with it.

Charbone Hydrogen (TSXV: CH | OTCQB: CHHYF) — Now Shipping, And I’ve Trimmed

Breaking: This morning Charbone announced that they are opening a 3rd hub in Albany. More to come

I sat down with Charbone CFO Benoit Veilleux for the second time, about six months after our last conversation. The headline: they are now shipping. Charbone has crossed from development and construction into distribution and sales, and management is now describing the company as a vertically integrated industrial gases business, ultra-high-purity hydrogen for semiconductors, data centers, and pharma, with helium and oxygen broadening the line. Three things I’m watching: Phase 1B at Sorel-Tracy commissioning in the next couple of months, which would push hydrogen capacity to roughly one ton per day; the Malaysia framework potentially shifting toward an accelerated project structure with equity participation for Charbone; and the Wolf River project in Wisconsin, where Charbone owns the Nadaro Dam and plans to self-produce electricity for hydrogen. Full disclosure on my position: I sold the majority of my position when the stock ran to 40 cents CAD. I still own some, and I’ll continue to add when the price is weak. The price ran ahead of the value on this one and I don’t leave money on the table when I don’t have to.

GOAT Industries (CSE: GOAT | OTCQB: BGTTF) — A Rough Patch, Honest Assessment

I’m not going to dress this up. The past month has been ugly for GOAT shareholders, and the stock is now trading in the ten-cent range. And now as of this morning they are halted. I would guess that is just until they get their audit done

Here is the sequence of events:

April 6, 2026 — WDM Chartered Professional Accountants resigned as the company’s auditor. Per the company’s filing, there were no reservations or modified opinions in WDM’s audit reports on the 2023 or 2024 financial statements.

April 10, 2026 — Horizon Assurance LLP appointed as successor auditor.

April 19, 2026 — Horizon resigned on its own initiative, only nine days after appointment. The company stated there were no “reportable events” between Horizon and GOAT.

April 27, 2026 — Steve Vanry resigned as Director and Corporate Secretary “to pursue other opportunities.”

Two auditor departures in thirteen days plus a board-level resignation is not a comfortable pattern, regardless of how clean each individual filing reads. I’m not going to tell you it’s fine. I’ll tell you what it is: a sequence of events that has materially shaken sentiment, and the share price reflects that.

The underlying thesis hasn’t changed — BetSource as the picks-and-shovels infrastructure layer for live sports prediction markets, with the patents, deployments, and partnerships still in place. What hasn’t shown up yet is reported revenue, and at this point that’s what would move the tape. Management’s communicated year-end projections, if delivered, would support a market cap materially above where the stock trades today. That word if is doing a lot of work — and it’s the whole reason the stock is where it is.

I am holding. I am not adding here, and I am not selling here. This is a high-risk corner of the market, and the right behavior in a high-risk corner is to size for the possibility you’re wrong, not just the possibility you’re right. Anyone who is overweight enough to be losing sleep should be honest with themselves about that. A longer GOAT-focused piece will follow once we have hard numbers to discuss.

LibertyStream Infrastructure Partners (TSXV: LIB | OTCQB: VLTLF) — Core Hold, Trade the Rest

This started for me as a swing trade and turned into something bigger. After it ran 5x earlier this year, I added a full position. My current approach: hold a core position, trade the majority around it. The past three months have been substantive on the operational side. In February, LibertyStream signed a definitive agreement with Select Water Solutions (NYSE: WTTR) to deploy commercial lithium carbonate production at Select’s water treatment sites in the Midland Basin, with the Stage 1 facility in Howard County, Texas scheduled for commissioning by end of December 2026 (capacity up to 1,000 tonnes per year of battery-grade lithium carbonate). They’ve since commenced production from the DLE Unit and the Lithium Carbonate Refining Facility at the Select site, pre-sold their first tonne, upsized a non-brokered private placement at $1.10 per Unit in response to investor demand, gained shareholder approval for Texas re-domiciliation in March, and added Michael Bodino to the board. December commissioning of the Stage 1 facility is the catalyst I’m watching. This is still a development-stage lithium company in a volatile commodity environment, the thesis depends on commissioning on time, producing to spec, and selling into a market where lithium pricing has been anything but predictable.

Medicenna (TSX: MDNA | OTCQX: MDNAF) — On the ASCO Stage in May, Real Data in H2

Big news on this one: Medicenna will be on stage at ASCO 2026 in Chicago on May 31. Highest-profile oncology meeting in the world, and visibility there matters for a small-cap immunotherapy name. What’s being presented, and what isn’t, matters, so I want to be precise.

The poster is a trial-in-progress presentation (ASCO abstract number TPS9612) on the NEO-CYT trial — the randomized neoadjuvant Phase 1b study testing MDNA11 in combination with nivolumab (anti-PD-1) with or without ipilimumab (anti-CTLA-4) in high-risk, surgically resectable Stage III cutaneous melanoma. The trial is sponsored by Fondazione Melanoma Onlus at the National Cancer Institute ‘G. Pascale’ in Naples, with Professor Paolo Antonio Ascierto, one of the most prominent melanoma oncologists in Europe, listed as the presenter. The poster goes up Sunday, May 31, 9:00 AM to noon CDT, in the Melanoma/Skin Cancers session.

A trial-in-progress poster presents the trial’s design, rationale, and endpoints — not patient data. So this is not a data readout. What it is, is high-profile validation: Ascierto presenting MDNA11 to the global melanoma oncology community in the field’s most-watched venue. That drives investigator interest, downstream conference invitations, and potential partnership conversations. For a name Medicenna’s size, ASCO visibility under Ascierto’s name is meaningful.

The actual data catalysts are still ahead, both expected in H2 2026: NEO-CYT interim data (first patient outcomes from the neoadjuvant melanoma study), and updated ABILITY-1 clinical results including data from the 2L/3L post-anti-PD1 expansion cohorts and the new NSCLC cohort the company added. There’s also an end-of-Phase 1 FDA meeting on ABILITY-1 planned for later in 2026, and the MDNA113 IND filing (their first-in-class PD-1 x IL-2 bispecific) is on the H2 2026 calendar.

Why I’m still long: the IL-2 space keeps validating itself through competitor M&A; Medicenna’s design (preferential CD122 binding, no CD25 binding, albumin scaffold for pharmacokinetics) is clinically differentiated; NEO-CYT is structurally clever because Fondazione sponsors it and Medicenna supplies drug (runway preserved); and the company is moving from “interesting science” to “multiple readouts on the calendar.” That’s the phase where small-cap biotech either rerates hard or breaks down hard, depending on the data. Clinical-stage biotech is binary, position size accordingly. I’m still long, still working to secure an interview.

LEEF Brands (CSE: LEEF | OTCQB: LEEEF) — Q1 Numbers Tomorrow

LEEF reports Q1 2026 financial results tomorrow, Wednesday, May 6, after the market close, with a 5:00 PM ET conference call led by CEO Micah Anderson, CFO Kevin Wilson, and CSO/IR Jesse Redmond. The webcast link is in the company’s release. This is the print I’m watching most closely this week.

The setup is interesting because of what’s happened in the past couple of months. On March 12, LEEF announced a US$4.5M initial closing of an up-to-US$8M financing led by Mindset Capital and its founder Aaron Edelheit (units at CAD $0.25 with warrants at CAD $0.30, plus preferred shares carrying a 15% annual dividend with a CAD $0.38 conversion price); Jamie Mendola joined the board in connection with the financing. Proceeds are earmarked primarily for expanding Salisbury Canyon Ranch to its full 180-acre permit size, which would make it one of the largest licensed cannabis farms in California. Then on April 16 the company announced the acquisition of Standard Holdings, parent of Himalaya Vapor, a California-based premium concentrates brand known for full-spectrum cartridges; the deal closed April 28, alongside the Q1 earnings date announcement.

Thesis is vertical integration: bring biomass production in-house at Salisbury Canyon Ranch, supply LEEF Labs’ extraction lines from the company’s own farm, compress input costs, and improve margins. If it lands the way management has framed it, that’s a structural margin story, not a cyclical one. Adding Himalaya on the consumer side gives LEEF another premium California retail line without rebuilding cultivation or extraction from scratch.

What I’m watching tomorrow: revenue trajectory versus prior quarters, gross margin direction (the cultivation expansion thesis is fundamentally a margin story), Salisbury Canyon Ranch construction timeline, and any color on Himalaya’s integration into the existing wholesale and retail mix. The conference call typically gives more than the press release on operational specifics.

Risks unique to this name. U.S. cannabis remains federally illegal, which carries through into banking, capital markets access, and especially IRS Section 280E, which disallows ordinary business expense deductions for cannabis operators and effectively taxes them on gross profit rather than net income. California specifically has had years of severe price compression and a large unlicensed market that competes directly with licensed operators. LEEF has been working through this — the company retired $10.5M of debenture debt ahead of its 2027 maturity in late 2025, removing over a million dollars a year in interest expense, but the underlying regulatory and market environment is what it is. High-risk corner of the market. Position size accordingly.

Swing Trade Update: AMFN (formerly RNWF)

When I introduced this in March at six cents, I told you I’d already been riding it from two to seven cents. I think the range is currently four to nine cents and may go higher. From there it dipped to .0396, ran to .0978, and is now sitting around .082 — I have completely exited my position. If it taps four to five cents again, I’ll buy back in. Rinse and repeat to stack those doubles. I am not in any way suggesting this company as an investment. It might be a good investment but I am only looking at the chart.

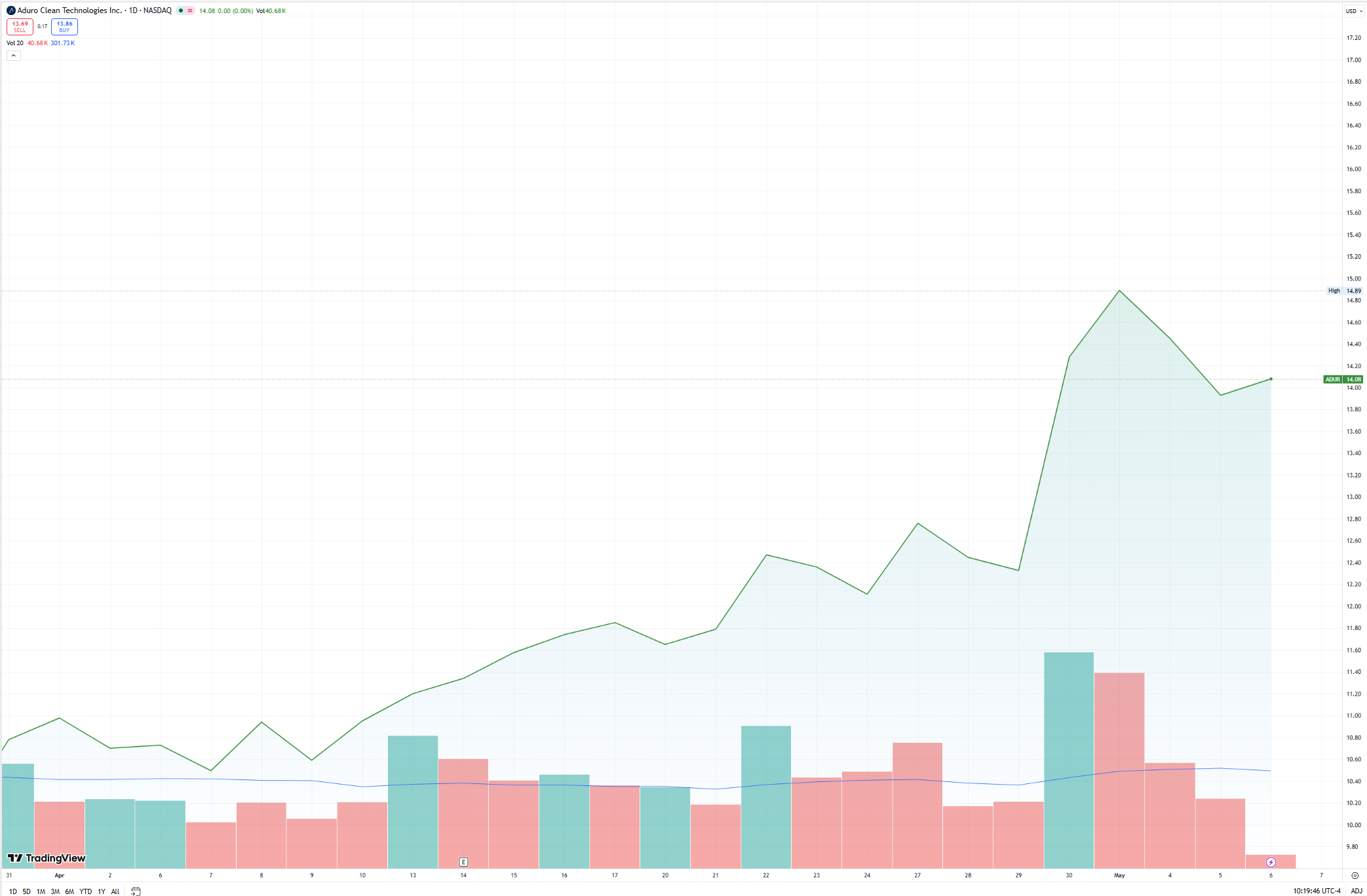

ADURO Expect a full article on Aduro’s freshly announced Uinta vertical. Below is the 30 -day chart and it looks like it is ready for another move. We had two back-to-back days with trading over 600k shares. People are starting to take notice.

Disclosures:

I am not a financial advisor, and this is not financial advice. I write about th3 stocks I hold and the trades I make for you educational and entertainment purposes. 45 Degrees is a related party to Penny Queen. 45 Degrees, Inc had been engaged by Rocket Doctor from commencing July 18, 2025, for a six-month term to provide advertising services including Google Ads, social media, and video interview distribution. 45 Degrees has been contracted by 1502655 B.C. LTD to provide advertising services for GOAT Industries commencing on 02/02/2026 at $30,000 USD per month for a period of 6 months. This article is not part of their contract.

Much appreciated, Penny. If you do manage to speak with Dr. Merchant, it would be instructive to know the impact that the new “fractional” CMO has had on the company’s trajectory so far; her consultant firm’s website seems heavily Merck-skewed……

Hi Penny, thank you for the updates and I really like your openness to discuss the real situation on the ground. I also appreciate all the interviews you do and find them to be very informative. Thank you!