LEEF Brands: Grown-Up Potential at a Small-Cap Price

First Harvest from the Ranch is Just Weeks Away—Here’s Why That Matters

OTC: $LEEEF | CSE: $LEEF

I’ve had a lot of people ask me what else I’m holding, and LEEEF is one of my top picks right now. I own a lot—enough that you could probably measure it in acres of their Salsbury Canyon Ranch.

The real catalysts for this company come later this year, when the impact of their cultivation operations starts hitting the books. But the pricing? It’s already compelling. They’re about to harvest their first 700,000 cannabis plants, and that shift from buying biomass to growing their own is going to dramatically reduce costs and expand margins.

This is a story about growing profitability in an unloved, but rebounding sector—and one where most peers trade at significantly higher multiples.

There’s a disclaimer at the bottom noting that I have consulting options. That creates a potential conflict of interest, and I won’t hide that. I bought this for the fundamentals, and I still think the best part of the story hasn’t even hit the numbers yet.

If Glass House is the blueprint for a vertically integrated, margin-efficient cannabis giant in California, then LEEF Brands is its younger sibling, stepping into their own with momentum, leverage, and now, direct collaboration.

Glass House has expanded significantly in cultivation and retail. LEEF is following suit with its own powerhouse asset—the 1,900-acre Salsbury Canyon Ranch—while dominating the concentrate niche and establishing a strategic partnership where Glass House now operates LEEF’s retail outlet and supplies them with trim.

This isn’t merely a handshake deal. It’s a signal that LEEF is maturing into a structure that the market already rewards—just at a significantly discounted price.

📋 Glass House vs. LEEF: Big Brother & Little Brother

Metric Glass House (GLASF) LEEF Brands (LEEF)

Market Cap $455M $27M

Revenue (2025e) ~$225M ~$30M

Adjusted EBITDA (Q1) $4.4M ~$1.3M

EBITDA Margin (Q1 ) 9.8% ~17%

Cost of Production/lb $108 ~$25 (bought) → $8–15 (own)

Cultivation Scale 1M lbs (targeted 2026) 2 crops from 65 acres (2025)

NY Expansion Gummies via Eaze Processing license (LOI)

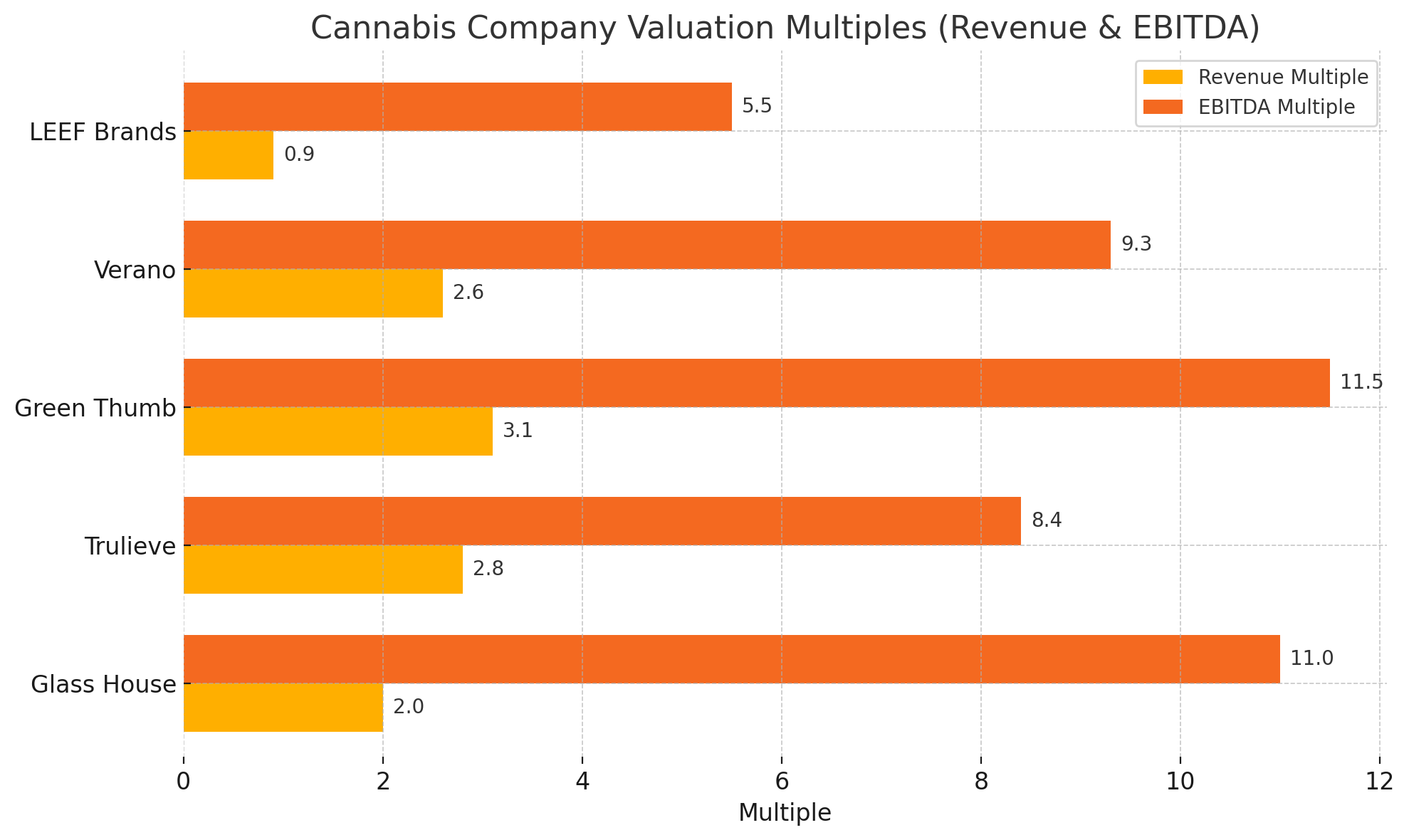

I chose GlassHouse for this comparison because they are the giants of the California market, one is clearly a gianter giant (yes, those are the words I’m choosing). Below are some other companies in the sector and their multiples.

🌿 The Ranch That Changes Everything

LEEF’s 1,900-acre Salsbury Canyon Ranch - valued at $40.8M USD - isn’t just a pretty asset. It’s a margin monster in waiting.

Currently, LEEF is buying input material at ~$25/lb. Once its crops come online (two harvests expected in 2025), they anticipate producing their material at $8–$15/lb. That cost reduction could more than double gross margins - and that’s before revenue growth from concentrate sales kicks in.

Unlike many cannabis companies relying on expensive third-party growers, LEEF’s vertical integration is real, imminent, and foundational to margin expansion.

🧠 Note: The ranch was independently valued at 40MUSD and isn’t currently valued at full market value on the books. Investors like the New York expansion and potential federal reform are getting it as a free call option, while the entire market cap of LEEF is 2/3rd the value of the ranch alone!!

💪 Extracting Value (Literally)

LEEF focuses on the number one player in California's concentrate market, rather than on California’s oversupplied flower market, where demand still outpaces supply. Their recent upgrades tell the story:

Ethanol extraction: +66% capacity

Solventless extraction: +50%

Hydrocarbon extraction: +38%

By investing in Concentrate infrastructure, LEEF is better positioned than most to monetize the post-harvest bottleneck - while others try to dump flower at a loss.

⬆️ Catalysts Ahead

Two Salsbury crops in 2025 - Materially lower cost of goods sold

New York license LOI - Entry into a $1.5B+ market; concentrates = 52% of products

Glass House partnership - Signal of strategic alignment, and a validation of LEEF’s infrastructure

Federal rescheduling or deregulation - Not priced in, but would unlock banking, listing opportunities, and interstate potential

Valuation reset - Even a 2x revenue multiple puts LEEF closer to $0.40, and that’s before margin expansion

🧶 What’s LEEF Worth? A Look at Revenue and Multiples

Currently, LEEF is trading at just around 1x revenue and 5.5x EBITDA. Compare that to Glass House, which trades at ~2x revenue and 10–12x EBITDA. That’s a serious valuation gap -, especially considering LEEF’s comparable or even stronger margin potential going into 2025.

Let’s break it down again.

Current Comparison

Metric Glass House (GLASF) LEEF Brands (LEEF)

2025e Revenue ~$225M ~$30M

EBITDA Margin (target) ~20% ~20%+ (Q1 estimated)

Market Cap ~$455M ~$27M

EV/Revenue ~2x ~0.9x–1.0x

EV/EBITDA ~10–12x ~5.5x

📈 Upside Scenarios

These following scenarios are my modelled estimates, not company guidance. They are based on potential margin expansion from owned flower, higher concentrate output, and entry into New York.

Scenario A - Ranch and NY Pay Off Early

Revenue: $50M

EBITDA: $10M (20% margin assumption)

2x Revenue = $100M market cap

10x EBITDA = $100M market cap

➡️ Roughly 4x from today’s valuation

Scenario B - They Keep Scaling

Revenue: $75M

EBITDA: $18.75M (25% margin assumption)

2x Revenue = $150M

10–15x EBITDA = $187M–$281M

➡️ 5x–10x upside from here

📌 Note: LEEF’s Q1 2025 EBITDA was estimated at ~$1.3M on ~$7.5M revenue, suggesting a ~17% margin. These modeled scenarios reflect potential improvement based on ranch production and NY operations.

🔁 So Why the Low Multiple?

Because the market hasn’t caught up yet. LEEF:

Doesn’t yet reflect revenue from its Salsbury Canyon Ranch (two 2025 harvests incoming)

Hasn’t priced in the New York market opportunity

Isn’t getting credit for a $40.8M ranch asset on the books

Still flies under the radar despite strong EBITDA margins

This is where I see the asymmetric opportunity......

You're paying today’s valuation based on what they've already built - and getting the ranch, the margin expansion, the New York upside, and the cannabis reform optionality as a free call option.

🎯 TL;DR

LEEF doesn’t need a miracle.

It just needs:

A couple of successful harvests

A strong NY entry

And a little attention

Then?

A re-rating to Glass House-like multiples could, depending on execution, elevate this from a $0.15–$0.20 stock to $0.40–$1.00, not considering any improvement in the sentiment of the Cannabis sector, which could propel the valuations of all companies in this space to multiples of their current trading positions (I still recall the days of 2016 to 2018 and 2020-2021 when Cannabis Companies were trading at 10 to 30X of forward-looking revenues!!)

I am long LEEF Brands. This is not financial advice. This content is for informational and educational purposes only. 45 Degrees, Inc. has received 300,000 options as part of a consulting agreement.