Great Expectations: Margin Expansion and Asymmetric Upside

Review on four big players in my portfolio

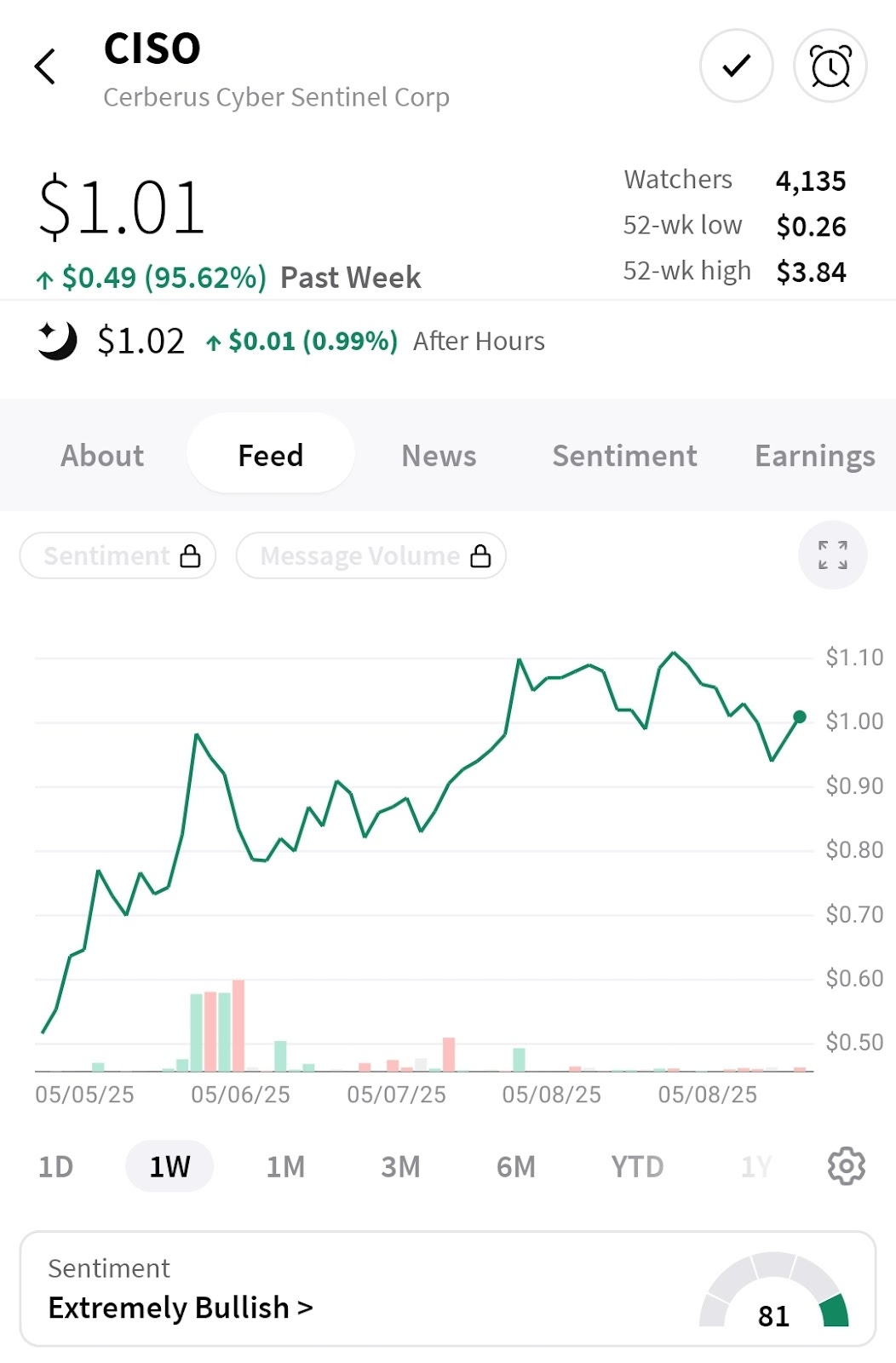

Show Me Your Margins: $CISO

After running up over 95% this past week and trading as much as 66 million shares - more than twice the entire 31 million share float - in a single day 😕, next week looks like it might be just as exciting. Sentiment has climbed and awareness is spreading fast.

We’re just a few trading days out from CISO Global’s earnings, and I, for one, could not be more excited about the margins. This is the part of the article where I get to do my favorite bit of psychic accounting - where we take what we know about the future, mix in what we know about the past, and try to come up with a likely range.

The task is, frankly, impossible.

Why? Because CISO sold off its low-margin Latin American operations, shedding both revenue and a hefty amount of debt. That makes modeling trickier - but in a good way.

What we know about next year:

CISO has guided for at least $34 million in adjusted EBITDA-profitable services revenue in 2025, along with $5 million in high-margin software bookings. Based on my recent interview with the CEO, he’s not just hopeful - they’re executing with confidence.

What we know from the past:

CISO’s revenue has traditionally been heavier in the back half of the year. It’s unclear exactly how much of that was from the Latin American ops, but if we look at 2022 - before those units were fully integrated - we see Q1 came in at $9.3 million, ramping each quarter to a Q4 high of $14.74 million. That’s more than a 50% increase from Q1 to Q4.

Back then, the company was running a higher-revenue, lower-margin model. I don’t expect them to hit those top-line numbers again right away, but I do believe the sales cycle is still similar, and we’ll likely see a similar ramp throughout the year.

But honestly… revenue isn’t the story here.

The real story is margin expansion. CISO has now completed the integration of 13 acquired services firms, paid off its highest-interest debt, and is pivoting hard into software offerings with ~75% margins. That means more of every dollar sticks.

I’ve had a few people ask what Adjusted EBITDA actually is. Here’s what it is and why it matters: it’s a way to measure profitability that leaves out non-cash expenses - things like stock-based compensation, which show up in accounting but don’t impact how much money the company actually keeps or spends. It’s especially helpful for companies like CISO that are growing fast and using stock grants to attract talent. The fact that those stock-based costs have been steadily coming down just adds to the bigger picture: they’re running a tighter, more focused business.

Add in the Cyber Assurance Group partnership, which targets the small and medium business (SMB) market with bundled cybersecurity and insurance products, and you’ve got real, sustainable growth momentum heading into 2025.

Give me a few quarters of increasing margins, followed by growing sales, and we’ll be staring down multiple expansion. The company has already rerated from ~0.3x to nearly 1x trailing revenue. And if margins come in as expected, this may just be the beginning.

And now, the chart:

The stock has been hanging out near $1.00, with clear resistance at $1.26, but volume and sentiment suggest we’re coiling for a breakout. I still see a clean path to my first target of $1.70, especially if margins come in strong and reaffirm the 2025 outlook.

If you're still doing homework, check out the Zacks piece that flew under the radar last week:

Zacks Small Cap Research - CISO: Leading cybersecurity provider entering new growth phase with high-margin, recurring revenue software offerings.

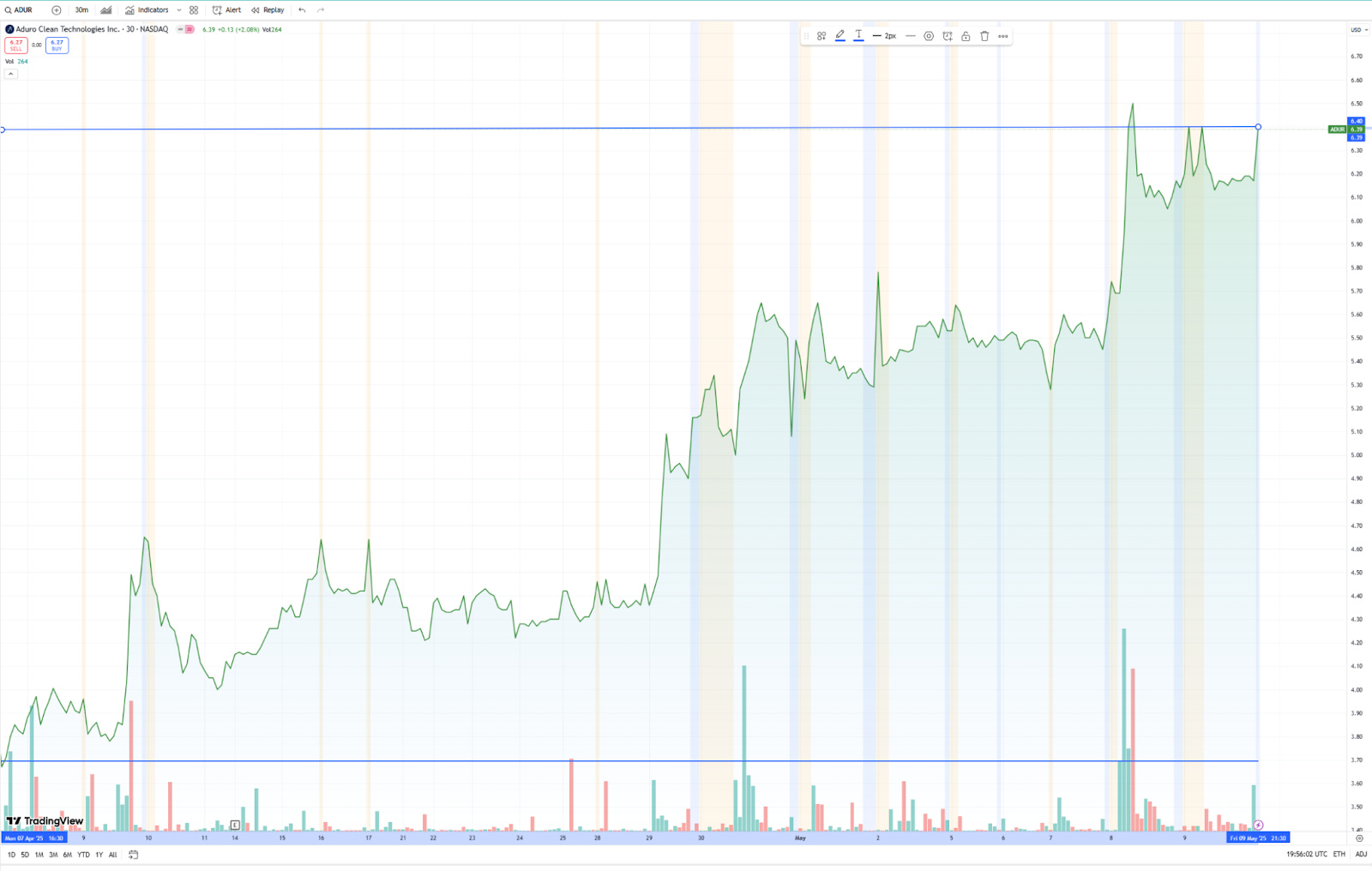

Aduro Clean Technologies: Quick Update + Must-Watch Panel

Over the past month, my plastic recycling ride or die, $ADUR, has nearly doubled off its recent bottom, closing after-hours Friday at $6.40 - forming a textbook cup. I’m personally expecting to see a breakout at $6.60 that could take it past its all-time high of $7.01, especially with all the new eyes coming to the stock and the Next Generation Pilot Plant coming in Q3.

We just dropped a very bullish panel discussion on YouTube - and I say that transparently: four long-term bulls, no bears. If you’re looking for balanced skepticism, this isn’t it. But if you want deep conviction and due diligence from shareholders who’ve done the work and have serious skin in the game, this is the one to watch.

The panel dives into:

Why dirty plastic is the real prize in recycling - and why Aduro can handle it when others can’t

How modular, on-site reactors change the economics of waste

Why landfills might become the new oil fields

What Siemens, Shell, CleanFarms, and Total see in Aduro

Why the stock may still be in its early innings, even after this recent run

You’ll also get a brilliant cost breakdown showing just how broken the current system is - and why Aduro may be the trillion-dollar solution hiding in a $170M market cap.

Watch the full panel here:

Reminder: Everyone on this panel owns shares. Do your own due diligence.

Charbone Hydrogen: Quiet News, Big Implications

While it didn’t spark much immediate price action, Charbone Hydrogen (US: $CHHYF - Canada: $CH) signed a USD $50 million construction term sheet back on May 1st - and that’s a big deal, even if the market is still snoozing on it.

Yes, it’s just a term sheet - so no guarantees, but here’s what matters:

The company currently has a market cap around 6m USD and a ~4 cent share price

The funding should support 5–10 phases, so not just one plant

Each phase = a new module - this is scale baked in

They expect to be profitable from the beginning, even with Phase 1 of Plant 1

They’re using plug-and-play electrolysis systems, reducing execution risk and speeding up deployment

Translation?

If this deal closes, Charbone moves from a small-cap green hydrogen story to a multi-location, revenue-generating clean tech company, with far more credibility and upside than today’s share price reflects.

For me personally, I own a lot of shares and will begin to ladder out a percentage as I approach a double, to reclaim some of my capital. At this point, I expect to let the bulk of my shares go on a much longer ride - this is the only pure play clean hydrogen stock out there. If Plant 1 performs as expected, it validates the model - and sets the stage for serious momentum.

LEEF Brands: Not My Usual Pick, But the Math is Too Good

LEEF isn’t clean tech or disruptive - it’s just a damn good deal. It’s a cannabis company, in a market that has punished cannabis stocks for years. But I keep coming back to it for one simple reason: the numbers make no sense - in the best way.

LEEF is a vertically integrated operator that consistently brings in over $30 million in annual revenue, has a strong wholesale business, and holds licenses across extraction, cultivation, and manufacturing. Most people still haven’t noticed that they’re sitting on a 1,900-acre, fully licensed ranch in Santa Barbara County - land that’s been independently valued at $40 million USD.

And no, that land isn’t on the balance sheet, which helps explain the market disconnect. The company’s current market cap is under $20 million. Let that sink in.

They are in the middle of growing their first crop right now - 700,000 plants expected to be waist-high by June, right as investor attention tends to rotate back to outdoor growers. These plants could reduce input costs for extraction from ~$25/lb to just $6–$12/lb. That means big margin expansion, and possibly a re-rating if the market finally starts pricing in the value beneath the surface.

If this wasn’t cannabis, it would be trading much higher based on land and revenue alone. But because it is, we get an undervalued, cash-generating company with asymmetric upside. I know it’s not my usual pick, but the math doesn’t lie - and I’m happy to hold this one while the market catches up.

Final Thoughts + What’s Next

As always, this is not investment advice. These are my personal opinions, shared to spark your own research and reflection. I hold positions in all the companies mentioned - CISO, Aduro, Charbone, and LEEF - and I don’t mind waiting when I believe in the margin expansion and growth trajectory.

Next week, I’ll be diving into Medicenna - what the latest data means, and why I doubled down just ahead of their Nasdaq delisting.

That's an absolutely fair point and I could have worded better. I am speaking specifically to the SBC, since it dropped 25% from 22 to 23 and another 20%, i think, from 23-24.

Great coverage but $lode didn't make the cut?